We hope that everyone is well and looking forward to the summer. It has been an interesting year, and we suspect we shall encounter a few more surprises as we head into the second half of the year. Market moves have been quick and rather dramatic. The violent and swift nature of both the March decline and the subsequent 2-week rally, that completely erased the decline. Many of the moves this year have been punctuated with overnight moves of historic proportion based on tweets, making it challenging to communicate our changing thoughts as we maneuvered through the last 2 months. However, we have successfully navigated both the drop in the markets and the subsequent rally.

As we highlighted in our last update, we reduced our equity risk by about 20% when the market broke the 200-day moving average. We were bullishly inclined before Iran and the pullback. We started buying on April 1st, and we invested most of that cash at good levels in companies we like. We still have a modest cash reserve that we will be using to add to themes we think will work well moving forward.

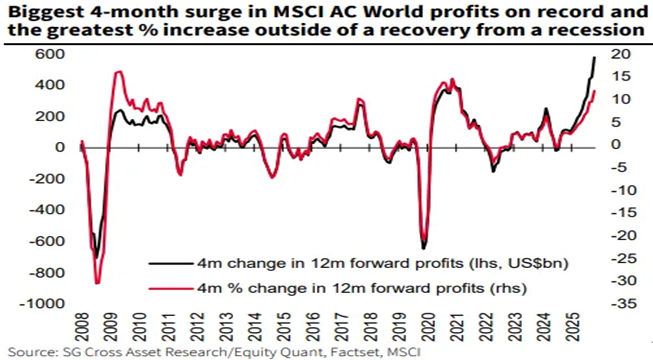

2026 has been a good year, so far! We have been building positions over the last 2 years in the companies that provide picks, shovels and materials, as well as the power and components that are the backbone of the massive AI buildout. Earnings from these companies have been strong, and the expenditure forecast for 2027 suggests that AI spending will increase by an average of 30% from current levels. Moreover, while valuations are rich, they are rich for a particularly good reason. Profits are surging at a rate of change that is now exceeding the Covid rally, which should provide the underpinning to help support stock prices moving higher.

We expect US stocks to hit fresh record highs in the months ahead.

- Per consensus estimates, the S&P 500 is projected to reach 7,600 by year-end, representing a 6% gain from prices on April 30th.

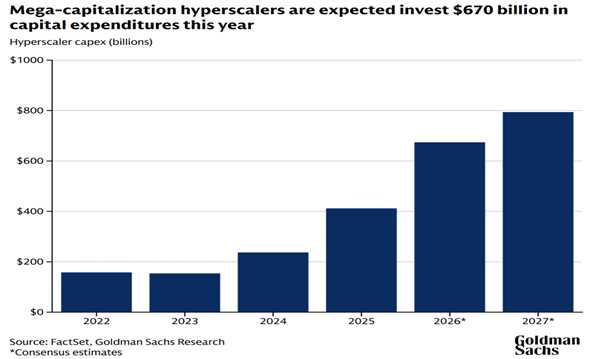

- AI investment is expected to drive roughly 40% of S&P 500 earnings growth this year, with the largest cloud computing companies planning to spend an estimated $670 billion in 2026.

- The market has staged a sharp rally of about 13% since late March, its sharpest rise since April 2020, fueled by improving geopolitical sentiment and rising corporate confidence.

With that backdrop, here is how we re-invested the cash we raised in the pullback.

We purchased new positions or added to holdings in the following companies:

Alphabet (GOOGL), Broadcom (AVGO), Amazon (AMZN), Morgan Stanley (MS), TeraWulf (WULF), Costco Wholesale (COST), and TJX Companies (TJX).

In ETF’s we purchased:

US Power Infrastructure (POWR), S&P 500 Momentum (SPMO), AI Power & Infrastructure (AIPO), Latin America (ILF), Brazil (EWZ), and Tortoise Energy (TNGY).

Collectively, this basket has materially outperformed the indices since we bought them in early April.

The fixed income market has been more volatile this year with uncertainty over private credit funds, and sticky inflation, with oil and deficits being the primary culprits. Looking ahead, both upside risks to inflation and downside risks to employment remain, pulling the interest rate outlook in opposite directions.

We anticipate that the Fed is on hold and will not cut rates unless the economy starts to falter. If the economy continues to expand, we could see a potential rate hike. Accordingly, we have reduced some of our interest rate duration and are investing in 3–5-year products with attractive yields and less rate risk. We are continuing to add to our municipal holdings as rates are attractive.

We are still optimistic that US markets will continue to climb higher into the year end. However, the uncertainty over the Iran situation is a factor which could slow the current pace of global growth, particularly in counties and regions that are more meaningfully impacted by the increase in oil prices. The US is relatively insulated, and South America has an abundance of oil and mineral wealth. Once we move through these Middle East issues, global markets will likely move higher. A negative caveat is that growth could be tempered if oil is above $90 into mid-summer; the impact from continued high oil would likely be more meaningful.

We are happy to discuss our thoughts.